Explain it to me like I am a 5-year-old: LIBOR

- ameyashanbhag

- Aug 31, 2020

- 4 min read

This post is meant for people who are completely new to Finance but want to have a basic understanding of the stock market. My aim here is to make the concepts easier and more understandable.

Why do we care about LIBOR:

Speaking in layman terms, when you approach a bank for a loan, they charge you an interest rate e.g. for getting a loan of $50,000, bank XYZ charges you 3.5% interest. Where do you think this 3.5% number come from? Credit card companies charge you interest rate if you don’t pay up your balances. Where does the interest rate come from?

All those numbers come from LIBOR. Speaking with more finance jargons, when you enter an interest rate swap agreement, payment from Party A to Party B is based on fixed-interest rate and payment from Party B to Party A is based on variable-interest rate. For eg. Bank ABC will tell XYZ that it will pay XYZ 4% of a notional amount while XYZ will tell ABC that it will pay ABC (LIBOR+1.5)% of the same notional amount.

Approximately US $350 trillion of outstanding business in different maturities is dependent on LIBOR. It is also used to understand the health of banking system and predict the future central bank rates.

People use LIBOR to hedge against their risk and to maintain a moderate risk portfolio but how and when they do it will be a little too complicated for this post.

Yeah, now that we understood how important LIBOR is and what it does to the world economy, let’s have a look at what exactly it is.

What is LIBOR:

It is a benchmark interest rate at which banks across the globe lend or borrow money from each other. It is calculated and published everyday by Intercontinental Exchange(ICE).

It is based on 5 currencies — US Dollar, Euro, Japanese Yen, British Pound and, Swiss Franc also provided for 7 maturities — overnight/spot, one week, one, two, three, six and 12 months which gives us a total of 35 combinations. So there are 35 LIBOR rates calculated and released every business day.

How is LIBOR calculated:

The ICE Benchmark Association (IBA) creates a panel of global banks for each currency. For e.g. BoFA, Barclays, Citibank, UBS etc constitute for US Dollar LIBOR. The selection process for the panels are conducted every year.

Every morning, before 11 a.m. GMT, IBA asks the respective panels one question, “At what rate would you be ready to lend or borrow funds to other banks”. So then the banks send their answers for each of the 7 maturities, confidentially.

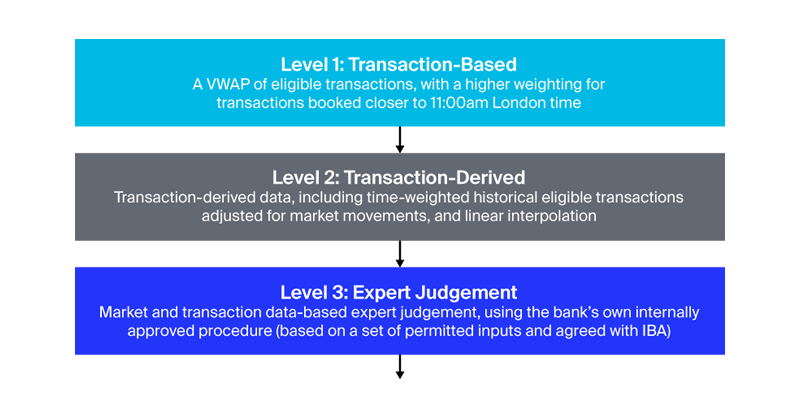

As of April 2018, the IBA submitted a new Waterfall Methodology for determining LIBOR.

First Transaction-Based Level: Taking volume-weighted average price() of all eligible transactions that the panel bank has given higher weighting for transactions closer to 11:00 am London Time

Second Transaction-Derived Level: If the panel bank does not have sufficient number of eligible transactions to make a Level 1 submission, take submissions based on transaction-derived data from panel bank.

Third Expert Judgment Level: If the panel bank fails to make level 1 and 2 submissions, it submits a rate at which it could finance itself with reference to unsecured, wholesale funding market.

Thomson Reuters then publishes the LIBOR rates along with the contributing rates that banks had provided, by 11:45 am.

Now that you know how it’s calculated, let’s take a look at how are we affected by it

Use Case Scenario:

So let’s say the LIBOR rate increases, which means banks want more interest if they are lending to some other banks. So if Bank ABC wants to borrow money from Bank XYZ ,then because of increase in the LIBOR rate, ABC will have to pay more e.g. 2% . So now customers who are planning to take out loans from ABC will have to pay more interest rate e.g. 5% The 3% difference here is the commission that ABC will keep with them.

Let’s have a look at the problems with LIBOR and it’s calculation.

What is wrong with LIBOR:

What do you think can happen when you select a handful number of banks and ask them to decide the LIBOR rate? Consider a scenario where you are reading through the wedding registry of a couple who are into games. You would find items like Xbox, PS4, Fifa 2020 etc.. basically they will try to get the gifts in their favor.

That’s exactly what happened in 2012. LIBOR lost its credibility after banks including Barclays, Deutsche and UBS were fined for manipulating LIBOR submissions. Banks have been reluctant to submit quotes on the basis of inactive market with the attendant risk of exposure to litigation.

LIBOR is also less of a robust, transactions-based market interest rate which makes LIBOR potentially unsustainable. As a consequence, the future of LIBOR beyond 2021 is uncertain. As USD LIBOR is used in large volume, it’s lack of sustainability can be a threat to the financial institutions and their systems. In order to prepare in advance, many countries have come up with an alternative reference rate. For example, U.S. has come up with SOFR, U.K. with SONIA, Japan with TONAR etc.

That’s it for this post. Do check out my other posts to gain more knowledge about finance. Please do let me know if there is any other concept in finance you want me to write an article on, I will try my best to explain it in simpler terms.

Also, feel free to ask questions in the comment section. Will be happy to help you out :)

Happy to connect on LinkedIn.

PS: The analogy I have used might not be 100% correct but it’s easy to understand things with a simpler analogy.

Source: Investopedia, SEC, Field Fisher, Thomson Reuters

Comments